Lenders know they are sitting on a lot of data. Your current accounts, credit cards, loans, savings, and even historic products all leave a trail of transactions behind them.

When we talk to credit, risk or product teams, we often hear that the data is there, but it is hard to use. Raw transactions sit in core systems in a format that works for processing payments, not for understanding people.

This is where internal transaction enrichment comes in. CaaS (Categorisation as a Service) is essentially our categorisation engine that takes raw data and turns it into structured information that teams can work with.

Once that happens, you can use the data you already hold to see how customers are really managing day-to-day.

In this post, we will look at what that process involves, where the most useful insight tends to appear, and how enriched internal data can support both growth and fair outcomes across your lending portfolio.

1. Enrich raw transactions into clear, workable insight

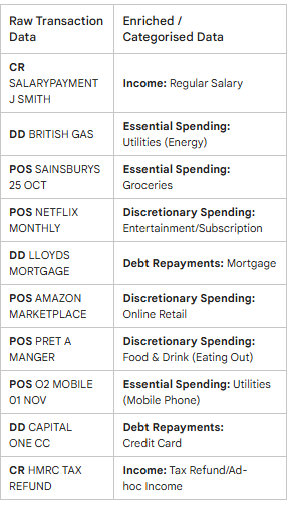

If you’ve ever looked directly at a raw transaction feed, you’ll know how quickly the usefulness disappears behind merchant strings, abbreviations and inconsistent descriptions. The value locked inside isn’t easy to interpret at scale. And that’s why enrichment is key

A categorisation engine, like AperiData offers, groups data into income, essential spending, discretionary spending, debt repayments, and dozens of practical subcategories. Creating something much more usable:

And because the process can run on data the bank already holds, there’s no additional action needed from customers, no change to onboarding flows, no interruption to existing journeys. It simply sits on top of internal datasets and organises them into something far more usable.

Once that structure is in place, new insights start to surface. For example, you can see how often income arrives, how stable it is across the year, and whether a customer relies on multiple sources. This is particularly valuable for people with variable incomes, where a traditional snapshot doesn’t give a comprehensive financial view.

Similarly, regular commitments begin to reveal repayment habits. You can see which obligations are paid consistently, which ones vary, and where customers may be stretching to meet several priorities at once.

With this insight, credit teams gain a clearer view of affordability. Risk teams see stress indicators earlier. And product teams understand behavioural trends that weren’t visible before.

In other words, enrichment helps an organisation to start making better use of the information it has held all along.

2. What structured behaviour tells you about customer needs

Once transactions are organised into clear spending and income patterns, the underlying behaviour becomes easier to see. This is where enrichment starts to move from analysis to practical value.

For instance, let’s take repayment behaviour. When the data is structured, you can see how someone approaches their commitments across the month:

- Some customers pay instalments early.

- Others spread payments out.

- And some rotate priorities when money is tight.

These help you understand which customers may need guidance before pressure turns into missed payments and which ones are managing well but could benefit from different product options.

| Repayment behaviour pattern | Transaction signal example | Lender insight |

| Pays early | Direct Debit for Loan ‘A’ consistently debits 3-5 days before the due date. | Financially well-managed; potentially eligible for better product offers or rate review. |

| Spreads payments out | Customer makes two smaller payments to Credit Card ‘B’ over the month instead of one large lump sum. | Prioritises full payment but manages cash flow tightly; low-risk of default but may need budgeting support. |

| Rotates priorities | Mortgage paid on time, but a smaller Credit Card minimum payment is frequently delayed or missed entirely. | Shows emerging financial strain/pressure; allows for proactive outreach before arrears build up. |

| Consistent | All regular commitments (Loan C, Utility D) are paid for the full amount on the exact same date each month. | Highly reliable borrower; demonstrates stable financial planning. |

And that’s not the only place strong signals appear. As you look across the data, you start to notice small changes that often precede bigger life changes:

- A rise in childcare costs might suggest a growing family.

- A cluster of furniture or homeware purchases might signal a recent move.

- Travel deposits or visa-related spend might indicate an upcoming relocation.

These moments aren’t always visible in other datasets, yet they stand out clearly once transactions are categorised.

These early clues are key because they point to where support, information or guidance can make a meaningful difference. When lenders see this information, communication becomes more relevant… and more welcome.

You also begin to see opportunities in the everyday patterns. Home-related spending can suggest interest in improvements, which naturally aligns with certain products. Regular payments to another credit provider might indicate a customer who would benefit from a balance transfer. And steady mortgage repayments over a long period could signal someone ready for a product review before their renewal date.

Essentially, this relies on treating behaviour as information. And when internal data is enriched, that information becomes clear enough to support timely, useful engagement rather than broad, unfocused outreach. As the behavioural picture sharpens, product journeys all start to feel more aligned to what customers actually need.

3. Strengthening support for customers at risk

As soon as spending and repayment patterns come into focus, you begin to see early signs of financial strain that would otherwise stay hidden until arrears appear. And this is where enrichment plays an important role in helping lenders support customers sooner.

Take income stability as an example. A single month of lower earnings might not mean much on its own. But when you can see several months of fluctuating deposits, or a change from regular salary to ad-hoc payments, it becomes easier to spot customers whose finances may be becoming less predictable. These are moments when a proactive check-in could prevent a small wobble from turning into prolonged difficulty.

Similarly, when categorisation highlights minimum payments on credit cards, frequent use of short-term credit, or growing spacing between regular commitments, it often signals that someone is finding it harder to juggle priorities. Recognising this early gives lenders the chance to offer practical support before arrears build.

You might also start to see subtle changes in essential spending. Rising grocery costs, changes in energy payments or an uptick in travel expenses can indicate broader cost-of-living pressures. Again, the value here is not in labelling customers, but in understanding what might be happening in their lives so that outreach feels timely and fair.

| Area of strain | Transaction signal/pattern | Lender insight & action |

| Income stability | Several months of fluctuating deposits or change from regular salary to ad-hoc payments. | Indicates less predictable finances. Allows for a proactive check-in to prevent a small problem from becoming prolonged difficulty. |

| Repayment behaviour | Categorisation highlights minimum payments on credit cards, frequent use of short-term credit, or growing spacing between regular commitments. | Signals difficulty juggling priorities and emerging pressure. Allows the lender to offer practical support before arrears build up. |

| Essential spending | Rising grocery costs, shifts in energy payments, or an uptick in travel expenses. | Suggests broader cost-of-living pressures. Helps in understanding the customer’s life so that outreach feels timely and fair. |

As you can see, all of this fits closely with the direction set by Consumer Duty, where the expectation is that firms should act before harm occurs. Enriched internal data helps make that possible. It gives lenders a way to identify risk earlier, tailor conversations more effectively and provide support that reflects the customer’s actual situation rather than relying solely on historical files or retrospective indicators.

And when customers do need help, internal data plays an important part in guiding the right approach. You can see when income stabilises again, when repayment patterns improve or when reliance on short-term credit begins to fall. This helps teams adjust plans in a fair and confident way, rather than relying on assumptions.

In the end, by understanding what is changing for customers, lenders can step in at the right time with the right kind of support.

See the value inside the data you already hold

Once you begin working with enriched transactions, you’ll see how much clarity was hidden in the data all along. Patterns that once sat buried in raw text become easier to read. Income steadiness, repayment habits, emerging pressures, and upcoming life events all form a picture that helps lenders make better, fairer decisions.

Even so, many organisations hesitate because they assume internal-data projects require significant time, budget or operational change. That hesitation is understandable. Large-scale transformation programmes can feel daunting, especially when teams are already stretched. But enrichment doesn’t have to start that way. A simple first step is often enough to show what the data can reveal.

How AperiData supports this work

Once lenders see what enriched internal data can reveal, the next question is usually the same: how do we make this practical? AperiData’s role is to make that step straightforward. Rather than adding complexity, the service is designed to sit inside existing processes and give teams the intelligence they need in a usable format.

What AperiData provides

Here’s a simple view of what the Categorisation-as-a-Service approach brings into the organisation:

| Area of support | What this means in practice |

| Transaction categorisation | Raw lines are organised into clear income, spending and repayment groups. |

| Affordability insight | Teams gain visibility of income stability, essential vs discretionary spending and regular commitments. |

| Behavioural patterns | Signals such as repayment habits, life-event indicators and short-term credit use become easier to spot. |

| Risk indicators | Emerging pressure appears earlier through changes in income flow or prioritisation of payments. |

| Flexible delivery | Works as a batch process, an integrated feed or alongside an existing Open Banking provider. |

Once the data is structured, the insight becomes much easier to use across credit, risk, product and customer support.

It’s easy to get started

Many firms begin with a simple test. AperiData enriches a sample of their current transaction data and produces a visual report that shows what the behavioural and affordability profile looks like once the noise is removed.

This allows teams to see:

- where early indicators of strain appear

- where lending opportunities might exist

- how income patterns vary across the portfolio

- which repayment behaviours stand out

- how different customer groups manage their spending

And because the insight comes from your own customer base, the findings tend to be both relevant and easy to action.

Some lenders choose to keep enrichment as a periodic batch process, especially when they want clearer portfolio insight without major technical changes. Others choose to surface enriched data inside their decisioning systems so that affordability and behavioural patterns remain current.

For organisations already using Open Banking, AperiData can simply sit beside the existing provider. The enrichment layer strengthens what is already there and helps create a consistent view of both internal and external transactions.

If you’d like to understand what enriched internal data could reveal in your own portfolio, we can run a sample and show you the insight. Just get in touch, and we’ll walk you through it.