Three major regulatory developments all centre on the same problem. The FCA’s mortgage rule changes in July 2025, BNPL regulation coming in 2026, and Ofgem’s energy debt relief proposals all reveal a gap in how we assess affordability.

It all comes down to visibility. (Or a lack thereof).

For instance, a borrower earns £60,000 with a clean credit file. They comfortably meet the 4.5x income multiple. By traditional measures, they’re solid. But what the assessment misses is three active BNPL accounts, energy bills that have doubled in six months, and £180 in monthly subscriptions. Their actual disposable income is half of what the paperwork suggests.

This is happening across UK lending right now. And regulators are acknowledging what transaction data has shown for years: traditional metrics tell you what someone should be able to afford. Whereas real-time data shows you what they actually can.

What changed in mortgage affordability in 2025

The FCA’s PS25/11 expanded the Modified Affordability Assessment in July 2025. (Previously, the MAA applied only when a new rate was cheaper than the current mortgage.) Now it covers situations where the new deal beats either the current mortgage or the existing lender’s retention offer. Essentially, this targets mortgage prisoners.

So, if someone’s successfully paying £1,400/month for three years, that’s meaningful evidence they can afford £1,200/month.

Additionally, the Bank of England withdrew its mandatory 3% stress test in August 2022. The FCA’s March 2025 guidance reinforced the flexibility lenders have in their approaches, noting that rigid stress testing sometimes blocks access to genuinely affordable mortgages.

Now, what does that tell us? If demonstrated payment behaviour provides better evidence than point-in-time calculations, what does that mean for affordability assessment generally? The MAA expansion hints at an answer: financial behaviour is key.

BNPL regulation and the visibility gap

Besides mortgage changes, third-party BNPL providers come under FCA regulation from 15 July 2026. The FCA’s CP25/23, published in July 2025, sets out the proposed regime. In it, the critical requirement was this: mandatory affordability assessments.

Over 10 million UK consumers use BNPL. The market added two million users in three years.

But here’s the assessment challenge: BNPL transactions are typically small, usually around £50, £100, maybe £200. And you can’t ignore that this might be someone’s seventh commitment this month, or that they’re juggling accounts across six different providers.

The issue is the cumulative exposure that’s invisible to traditional checks.

So, what does this mean for lending infrastructure?

Once BNPL is regulated and providers conduct proper affordability checks, those commitments become part of the lending picture. A mortgage applicant might carry £1,500 in monthly BNPL payments across multiple providers.

Currently, these often don’t appear on credit files until they go wrong. Traditional credit bureau data updates periodically and looks backwards. For BNPL (and increasingly for all lending) you need the current position.

That requires consented access to real-time transaction data. Which means Open Banking infrastructure becomes essential.

The cross-sector effect

When one lending category requires real-time affordability checks, it changes expectations across all lending. If BNPL providers can see complete financial position instantly, why would mortgage lenders rely on three-month-old bank statements?

Affordability considerations for energy debt and targeted relief

Now let’s look at UK households, who collectively owe £4.4 billion in energy debt. Ofgem’s proposed Debt Relief Scheme could write off up to £500 million for approximately 195,000 households.

Phase 1 targets customers on means-tested benefits who accumulated £100+ in debt between April 2022 and March 2024.

But here’s the problem: benefit status is a crude filter. Not everyone receiving benefits is in financial distress. Meanwhile, working households just above benefit thresholds might be severely stretched.

The challenge then is identifying who genuinely needs relief versus who qualifies by category.

The good news is, real-time visibility into income and expenditure patterns provides a more accurate picture than categorical eligibility. You can see actual affordability, instead of assumed affordability.

As our Commercial Director Nicola Dunn recently highlighted, “combining means-testing with Open Banking insights makes debt relief more targeted and effective. Real-time affordability data allows suppliers and advisers to identify early signs of stress and offer support before debt escalates.”

For energy suppliers, this aligns with broader obligations around avoiding foreseeable harm. Proactive identification of customers at risk enables earlier intervention, which is better for customers and better for suppliers managing arrears.

💡 Here’s what we’re seeing: Traditional eligibility criteria is giving way to a data-driven assessment of actual financial position.

Here’s what we mean by this…

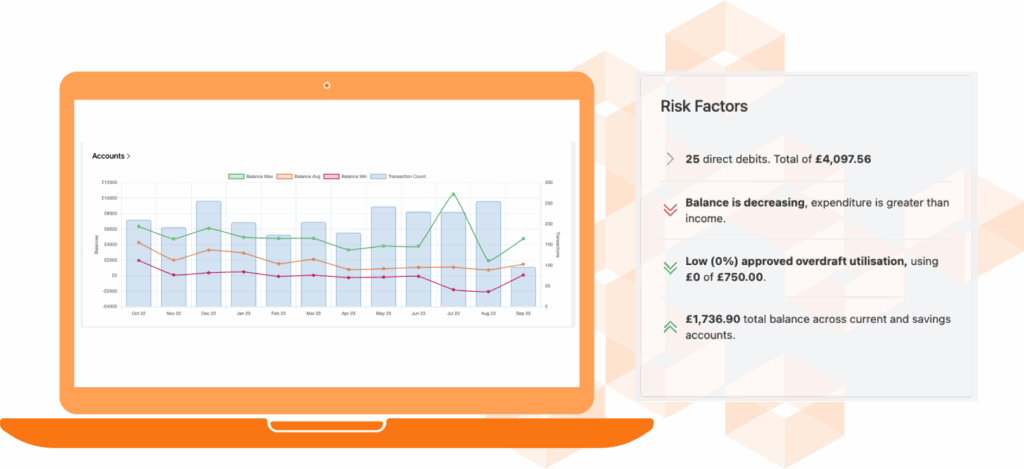

The real affordability picture: what transaction data reveals

When it comes to standard affordability assessments, they often rely on gross income from payslips, declared committed expenditure, credit file data, estimated living costs, and income multiple limits. However, transaction data shows what’s actually happening.

Here’s how:

1. Real-time commitment visibility through Open Banking

Direct debits that weren’t declared. Subscription services customers themselves have forgotten about. BNPL payments across multiple platforms. Payday loan usage. Overdraft reliance patterns.

These are the monthly outgoings that reduce disposable income but often these don’t appear in traditional assessments.

2. Transaction-based spending pattern analysis

Is expenditure stable or volatile? Are there signs of financial stress, such as rising credit use, late payment fees, or overdraft charges? How much genuine disposable income remains after essential spending? Are there seasonal patterns affecting affordability?

Transaction data answers these questions. Self-declared expenditure estimates don’t.

3. Automated income verification with banking data

Confirmed income actually hitting accounts. Regularity of income, which matters particularly for gig economy workers. Multiple income streams that might not appear on primary payslips. Benefits and other sources.

4. Machine learning for transaction categorisation

Raw transaction data is overwhelming. A typical consumer has 150-200 transactions monthly. Manual review at scale isn’t feasible.

That’s why machine learning becomes essential. Automated categorisation, merchant identification, and pattern recognition turn transaction noise into affordability signals.

5. Open Banking infrastructure requirements for lenders

This requires secure API connections to banking data, ML-powered categorisation engines, automated risk flag identification, real-time processing capability, and robust consent management frameworks.

So what’s the decision? For lenders, the choice is to build this capability in-house (typically 18-24 months, with significant ML expertise required) or to partner with providers who’ve already solved these problems. With BNPL regulation 18 months away and Consumer Duty already in effect, the decision timeline is compressed.

What an effective affordability assessment looks like in 2026

Three scenarios show the approach moving from traditional to real-time affordability assessment.

| Scenario | Traditional approach | Real-time approach |

| Remortgage Application (MAA) | Request 3 months’ statementsManual reviewConservative assumptions3-4 week timeline | Customer consents to Open BankingAutomated transaction analysisActual spending patterns visibleDecision in minutes |

| BNPL Purchase (Post-July 2026) | Limited visibilitySingle-provider viewDelayed commitment visibility | Real-time affordability checkMulti-provider BNPL visibilityCumulative exposure calculatedInstant decision |

| Energy Debt Support | Benefit status checkCrude targetingReactive approach | Transaction pattern analysisIncome drop identifiedProactive interventionEarlier support offered |

The common thread: Each scenario demonstrates how real-time data enables faster, more accurate decisions based on actual financial behaviour rather than estimates.

Next steps for affordability compliance

As we’ve discussed, in 2026, three separate regulatory developments—mortgage rules, BNPL regulation, and energy debt relief—are reaching similar conclusions about affordability assessment.

Disposable income is no longer “income minus declared commitments.” It needs to account for traditional credit (mortgages, loans, credit cards), BNPL payments (becoming regulated, increasingly visible), energy costs (especially relevant given recent volatility), subscription services (collectively material), and actual spending patterns and trends.

These elements don’t all appear on traditional credit files. They do appear in transaction data.

Better data enables more accurate decisions. That can expand access for creditworthy customers who look risky on paper but show positive behaviours in their transaction history.

The Government’s Financial Inclusion Strategy, published earlier this year, specifically highlighted Open Banking as a route to improved credit access for those with thin or impaired credit files. Because consented transaction data allows lenders to see beyond limited credit history to assess actual financial management capability.

Want to understand how real-time Open Banking data transforms affordability assessment? Contact our team.