Collections strategies have come a long way. But many still rely on the same assumptions: that customers can always repay, that circumstances stay the same, and that one-size-fits-all is good enough. Today, that’s a risky approach.

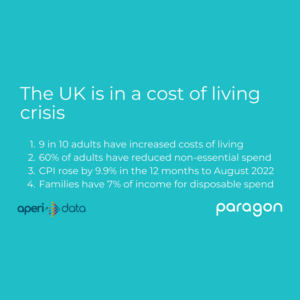

Rising living costs and income instability mean the gap between what people should be able to pay and what they can actually afford is widening. And with regulators placing more focus on supporting vulnerable individuals, lenders and other credit providers need to do more.

In this blog, you’ll see how Open Banking improves engagement, supports better outcomes, and boosts recovery rates. Plus, we’ll share an example of how this is working in practice.

The limits of static collections models

Traditional collections journeys were built with simplicity in mind. One route in, one route out. Everyone treated the same, regardless of what’s actually going on in their financial lives.

The problem? This kind of static model leaves no room for context.

Some customers are dealing with temporary setbacks, others are in long-term financial difficulty, and some have incomes that change month to month. Yet most strategies still apply the same rules, repayment plans, and contact cycles across the board because the data driving them is often outdated, patchy, or too high-level.

For example, a customer who’s missed a payment due to an irregular payday might receive the same tone of messaging—and face the same recovery timeline—as someone in long-term financial difficulty. These false equivalences cost businesses time, strain customer relationships, and reduce the chances of successful engagement.

This leads to a few familiar problems:

🛑Repayment requests that don’t match someone’s real affordability

🛑Escalation too early, or too late

🛑Support offered too generically to be useful

Worse still, these approaches can further push vulnerable customers into difficulty—and expose lenders to reputational and regulatory risk.

What Open Banking for collections adds to the picture

To build a collections strategy that adapts to the real world, you need data that reflects the real world. That’s where Open Banking for collections comes in.

By analysing live bank transaction data—with consent—lenders can see a far more detailed and accurate picture of someone’s financial situation. Not just credit history or balances, but what’s actually happening in real time.

This includes:

- Income patterns: regularity, sources, and stability

- Spending behaviour: essential vs non-essential, signs of financial stress

- Vulnerability indicators: benefits income, gambling transactions, persistent overdraft use

With customer consent, Open Banking allows lenders to securely access up to 12 months of real-time bank transaction data. Unlike static credit files, which may be 30–60 days old and miss important spending trends, Open Banking shows what’s happening now—giving you more reliable signals for collections decisions.

Similarly, this kind of insight changes the way you can segment your customers. Instead of broad, reactive categories, you can group people based on actual affordability and financial resilience. Who needs immediate support? Who could manage a repayment plan if it was flexible? Who’s showing signs of hardship that haven’t been flagged anywhere else?

Because AperiData is a regulated CRA, the data also meets high standards of governance and reliability—so you can use it with confidence, across the full lifecycle.

It’s smarter, more informed, and ultimately more human.

Smarter segmentation = Better engagement

Once you have a clearer view of your customers and what they can manage, you can start shaping collections journeys around them—not the other way around.

That might mean:

- Offering flexible repayment options to those with irregular income

- Prioritising early intervention for customers showing signs of vulnerability

- Adjusting tone and timing based on someone’s current financial resilience

It’s one thing to adjust the messaging. It’s another to rethink how the journey works from end to end. Who gets contacted, when, and how. What kind of plan they’re offered. How support is framed. And even when recovery should pause entirely.

For instance, one customer might show regular salary deposits and recent short-term borrowing—suggesting a need for short-term flexibility. Another may rely on benefits and show signs of persistent overdraft use, signalling deeper financial vulnerability. A third might have seasonal income patterns, calling for a repayment structure that adjusts over time.

We’re already seeing financial services firms use Open Banking for collections to move from blanket strategies to tiered journeys built around real needs: “As the technology moved forward and digital engagement has increased across the collections landscape, the ability to drive further personalisation continues to be enhanced and should be a key focus for collections operations,” says Martin O’Donnell, Co-Founder & CPO at DebtStream.

“Open Banking is another key factor to support this, real-time assessments of a customer’s circumstances allow you to understand the customer’s situation on another level, opening up opportunities such as personalised flexible repayment plans through to supporting identification of the right support for a vulnerable customer. I still feel Open Banking is still only getting started, and we’ve barely scratched the surface of how this can be used to support customers.“

The result? Fewer dropouts. More constructive conversations. And a better experience for customers, even in difficult circumstances.

The payoff – for customers and for you

When collections strategies are based on real insight, everyone benefits.

For customers, it means:

- ✅Repayment plans that reflect what they can actually afford

- ✅Earlier access to support before problems escalate

- ✅Fewer generic messages, more relevant options

For your business, it means:

- ✅Higher engagement and response rates

- ✅Stronger recovery performance

- ✅Reduced risk of regulatory breaches or complaints

There’s also a reputational upside. In a market where trust is easily lost, a fair and supportive collections process can set you apart. It shows customers—and regulators—that you’re serious about treating people fairly.

With the FCA’s continued focus on fair outcomes and vulnerability, lenders need data that can stand up to scrutiny. Transparent, tailored collections strategies reduce complaints and lay the groundwork for long-term trust.

Here’s just one example of how Open Banking for collections makes a difference. ⬇

Real-world results: How DebtStream and AperiData improved collections outcomes

AperiData’s partnership with white-label collections provider DebtStream shows what’s possible when real-time data meets smart digital journeys.

By integrating Open Banking insights directly into DebtStream’s self-service platform, clients saw big improvements in customer support and collections performance.

✅ 34% higher repayment plan sustainability for online journeys compared to call centre-assisted setups

✅ 92% of financial assessment data points automated, cutting down friction and speeding up support

✅ 97% authorisation rate for Open Banking payments, compared to just 80% for card payments

✅ Better vulnerability identification, with high-risk behaviours like gambling proactively flagged and linked to personalised support

Open consent also enables continuous monitoring, so repayment plans stay aligned to real affordability—not just what was true at the start.

The result? Faster assessments. More flexible plans. And a fairer, more effective experience for customers navigating financial difficulty.

Open Banking for collections: Smarter collections start with smarter data

One-size-fits-all collections strategies are outdated and ineffective. They miss the nuances that make all the difference: who can pay, who’s struggling, and who needs a different kind of conversation.

Open Banking for collections gives you the data to close that gap. With real-time insight into income, spending, and vulnerability, you can build collections journeys that are fairer, more efficient, and better for everyone involved.

Whether you’re trying to improve engagement, reduce complaints, or increase recovery rates, the starting point is the same: better data, applied with care.

Want to see how other lenders are doing it? Talk to us about how AperiData’s Open Banking insights are helping financial services teams create more effective, insight-led collections strategies.