Open Banking showed what’s possible when consumers gain secure access to their financial data. From faster lending decisions to smarter money management tools, it has proven the value of data sharing in everyday finance.

Fast forward to now, Open Finance promises to take that principle beyond current accounts, covering savings, pensions, mortgages, insurance, investments and more. The aim? To create a joined-up financial ecosystem that empowers consumers and businesses alike.

The issue is that with a broader scope comes greater complexity. More datasets, more stakeholders, and more risks to manage. In fact, recent discussions led by the FCA have made it clear that Open Finance will only succeed if it is built on reliable, standardised and trusted data foundations.

| What this blog covers > The move from Open Banking to Open Finance and what’s driving it. > The opportunities on the horizon from financial wellbeing to digital identity. > The challenges ahead why trust, interoperability, and data quality are make-or-break. > The role of regulated CRAs like AperiData in laying the reliable data foundations that Open Finance depends on. > Lessons from Open Banking, Expert opinion from Marie Walker at Raidium |

The promise of Open Finance

For consumers, Open Finance could mean a single, real-time view of their financial world, bringing together everyday spending, savings goals, pensions, and credit commitments into one clear picture. This should make it easier to plan for major life events, avoid financial shocks, and access products that are truly suited to individual circumstances.

For businesses, the opportunities are just as important. Lenders will be able to make faster, fairer decisions by seeing the full context of a customer’s financial position. Utilities and local authorities could identify vulnerable households earlier and provide the right support. And insurers and investment providers could tailor services with far greater accuracy.

That future is now closer than many realise. Momentum around Open Finance has accelerated in recent months. The FCA has now announced a new partnership with Raidiam to deliver the Smart Data Accelerator.

Marie Walker, Open Futurist, at Raidiam, explains the significance: “The recent partnership between the FCA and Raidiam for the Smart Data Accelerator programme demonstrates how critical collaborative testing is to realising this potential.”

She continues: “Through industry sprints and sandbox environments, we’re creating safe spaces to rigorously test product ideation, governance frameworks, and technical standards before they go live.”

This live testing environment allows firms to simulate and test real-world data sharing. Two new TechSprints, focused on mortgages and SME finance, will follow later this year. These initiatives mark the shift from concept to implementation and highlight how essential reliable data infrastructure will be in bringing Open Finance to life.

The FCA’s recent Open Finance Sprint pointed to four priority areas where this change could make the most impact:

- financial wellbeing

- financial growth

- financial resilience

- and digital identity and verification.

The aim is a more inclusive, responsive, and consumer-centred financial system. The vision is ambitious, but, of course, ambition alone won’t make it a reality.

Marie emphasises why this approach matters: “This ensures that smart data solutions deliver real benefits—fairer access to services, genuine competition based on quality rather than data lock-in, and stronger protections for vulnerable consumers.”

She adds: “By getting governance and interoperability right from the start through collective experimentation, we can accelerate innovation that truly serves UK consumers and businesses, moving smart data from promising policy to trusted practice.”

The challenge: making data usable, portable, and trusted

Turning the vision of Open Finance into reality depends on the quality and accessibility of the data that underpins it. If data remains siloed, outdated, or inconsistent, the ecosystem risks becoming fragmented and confusing rather than empowering.

Of course, consumers will only share their information if they believe it is secure, used transparently, and provides clear benefits in return. This makes trust critical for Open Finance. Without it, even the most sophisticated technology will fail to gain traction.

Similarly, standardisation is also key, because for Open Finance to work across banks, insurers, pension providers, utilities, and beyond, data needs to be portable and comparable. And interoperability (the ability for systems to “speak the same language”) will determine whether the experience feels seamless or disjointed.

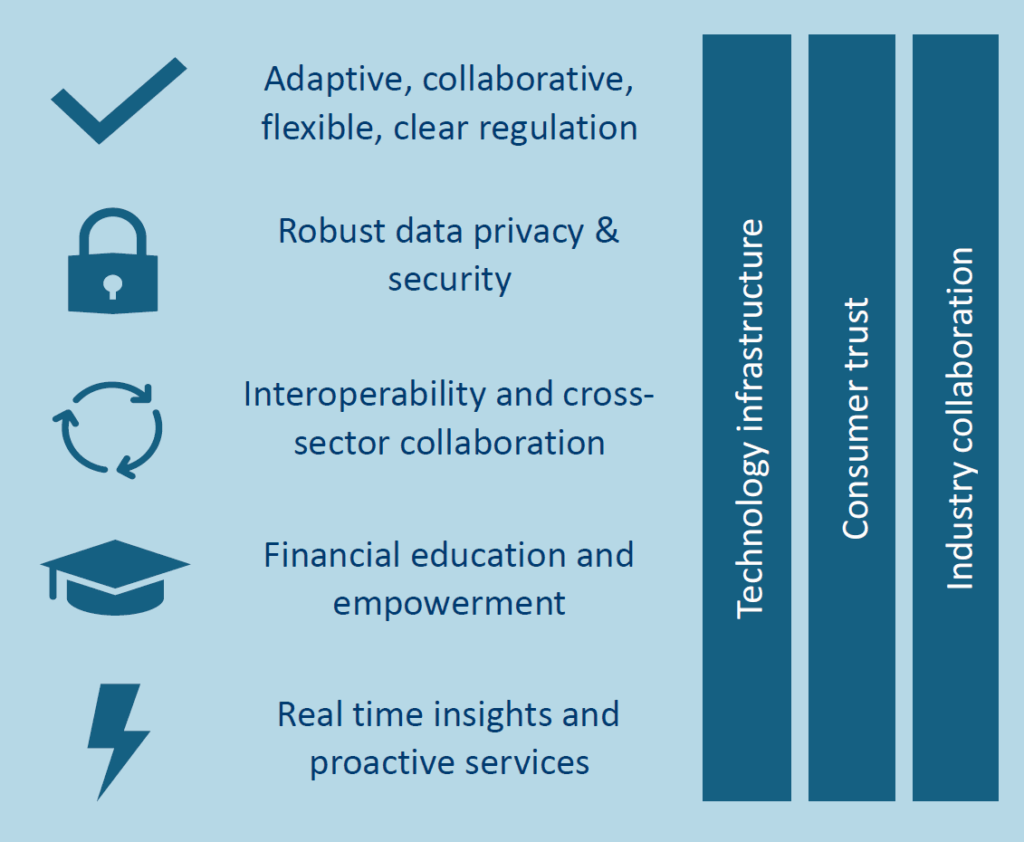

Interestingly, the FCA’s recent Open Finance Sprint set out five pillars that capture these challenges clearly:

- Adaptive, collaborative, clear regulation: rules that can flex with innovation, but still protect consumers.

- Robust data privacy & security: safeguarding consumer trust at every step.

- Interoperability and cross-sector collaboration: ensuring systems, standards, and industries connect rather than compete.

- Financial education and empowerment: giving individuals real control over their data and the confidence to use it.

- Real-time insights and proactive services: moving from static reporting to timely, actionable intelligence.

[Source: FCA Open Finance Sprint 2025]

These pillars are supported by three enablers: strong technology infrastructure, consumer trust, and industry collaboration. Without them, Open Finance risks becoming a patchwork of initiatives rather than a coherent, trusted ecosystem.

For the industry, the next thing to consider is how quickly we can build the foundations to support them. That’s where we can help.

Where regulated CRAs like AperiData come in

Meeting the challenge of Open Finance requires trusted intermediaries who can turn raw data into reliable, usable insights. That’s where regulated credit reference agencies (CRAs) have a key role to play.

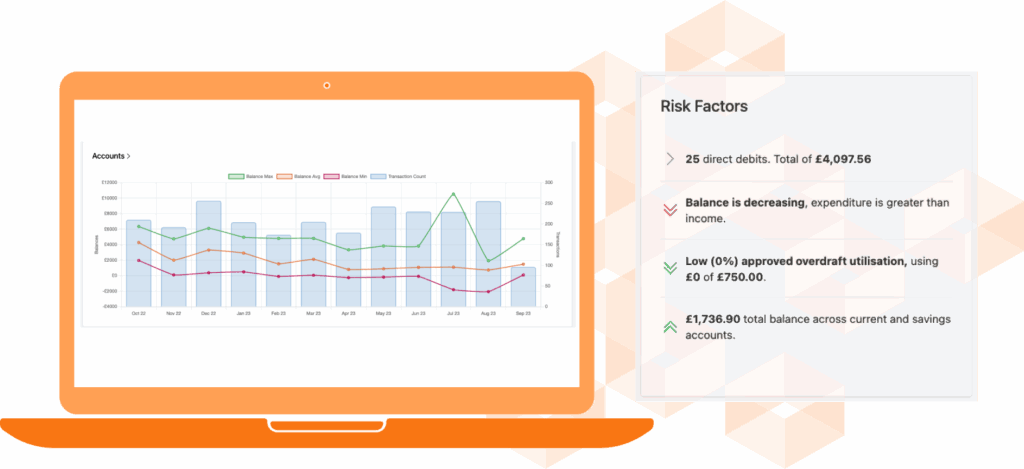

As a regulated CRA, AperiData is already working at the intersection of real-time financial data, consumer protection, and affordability. We focus on the very areas highlighted as priorities for Open Finance:

- Affordability and collections: using live transaction data to help lenders and utilities assess what customers can genuinely afford, reducing risks and supporting financial wellbeing.

- Resilience and vulnerability detection: spotting signs of financial strain early, enabling businesses and local authorities to offer timely support.

- Fraud and identity: supporting secure verification and reducing the risk of account takeover through transaction monitoring and categorisation.

| What sets AperiData apart is the combination of regulated status, real-time insights, and agility. While traditional CRAs provide valuable credit file data, AperiData closes the gap between static, retrospective information and the everyday financial reality that Open Finance depends on. |

This is what reliable data foundations look like in practice: regulated, standardised, and trusted.

Lessons from Open Banking (and the road ahead)

The UK’s Open Banking journey shows how much coordination is required to stand up a functioning ecosystem. Common standards, oversight committees, and industry-wide governance were all essential in creating consistency and trust. Open Finance will require the same (if not more), given the wider scope of products and providers involved.

Phasing will be key. Industry voices suggest that extending first to savings accounts, ISAs, and lending products makes sense before broadening out to pensions and insurance. Meanwhile, the development of pensions dashboards highlights how complex but valuable multi-party data integration can be, offering consumers a single view of their retirement savings.

For firms, Open Finance offers a chance to rethink services, test innovations in regulatory sandboxes, and prepare business models for a world where real-time data is the norm.

Building Open Finance on solid ground

The move from Open Banking to Open Finance is already underway. Roadmaps are being drawn, pilots are being tested, and the opportunities are clear. But the success of Open Finance will depend on whether consumers, businesses, and regulators can trust the data at its core.

That’s why reliable, standardised, and real-time data foundations matter so much. Without them, the promise of Open Finance risks collapsing under its own complexity. With them, the vision of a more inclusive, resilient, and empowering financial system can become reality.

With initiatives like the Smart Data Accelerator and industry collaboration already underway, the groundwork for Open Finance is being built. The next step is ensuring the data powering it is as reliable as the systems themselves.

At AperiData, that’s the role we play: helping organisations make better affordability and resilience decisions today, while laying the groundwork for the open financial ecosystem of tomorrow.

Ready to prepare for Open Finance?

Or if you still have unanswered questions, you might like our most frequently asked questions below.

FAQs on Open Finance

Q: How is Open Finance different from Open Banking?

Open Banking covers access to payment accounts and transaction data. Open Finance broadens the scope to include products like savings, pensions, mortgages, insurance, and investments, creating a fuller picture of a consumer’s or business’s financial position.

Q: What’s the biggest barrier to Open Finance?

Trust and interoperability. Consumers need to know their data is secure and used transparently, while firms need consistent, standardised data that can move across systems and sectors without friction.

Q: Who are the key players in making Open Finance happen?

Regulators (like the FCA and HM Treasury), financial institutions, fintechs, technology providers, consumer groups, and regulated CRAs such as AperiData, who turn raw financial data into reliable insights.

Q: What role does AperiData play in Open Finance?

AperiData provides regulated, real-time transaction data that supports affordability, resilience, vulnerability detection, and fraud prevention. By closing the gap between static credit data and everyday financial reality, AperiData helps build the foundations Open Finance needs to succeed.

Q: When will Open Finance become a reality?

The FCA is due to publish an Open Finance roadmap by 2026. In the meantime, industry pilots and regulatory sandboxes are already testing use cases, meaning the building blocks are being laid now