Local authorities can’t afford to rely on outdated assumptions when assessing financial hardship. Static indicators, like postcode, benefit status or historical income, only tell part of the story, and they miss the nuances of day-to-day financial strain.

What’s missing is a way to understand residents’ financial situations as they really are—right now. That’s where Open Banking comes in.

With permissioned access to real-time transaction data, local authorities can make faster and fairer decisions based on how people are actually managing their money in the present (not three or six months ago). That means more accurate assessments, earlier intervention and a better way to prioritise limited resources.

In this blog, we’ll look at the common challenges local authorities face when assessing vulnerability and how Open Banking data helps fill the gaps—while also supporting broader digital transformation goals.

The challenge: Knowing who really needs help

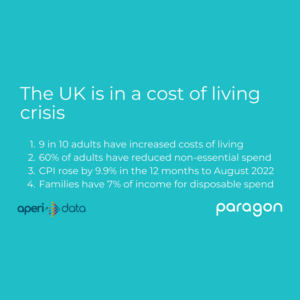

Despite the growing demand for support services, many local authorities still rely on fragmented or outdated data to assess financial hardship. That’s not through lack of effort—it’s down to the limitations of the information available.

Affordability assessments often rely on static or proxy indicators, such as postcode, council tax band, or benefit status. But these only offer a snapshot in time and often an incomplete one. This means a support model is built on assumptions which don’t always reflect the lived reality of financial strain.

Some of the most common issues include:

❌Outdated income information: Benefit data or income assessments may be months old, with no visibility of recent changes in employment or income drops.

❌Gaps in expenditure insight: There’s rarely visibility into outgoings like rent, childcare, debt repayments, or energy costs, which are key drivers of financial pressure.

❌Limited view of informal income or irregular pay: Zero-hours contracts, gig work and self-employment often fall outside traditional reporting methods.

❌Inability to spot early signs of distress: Without day-to-day spending insight, it’s hard to flag residents who are just about managing—until they reach crisis point.

❌Manual processes that slow things down: Vulnerability assessments are often time-consuming, relying on self-declared information or retrospective checks.

The result? Residents fall through the cracks, budgets are stretched thin, and councils risk missing opportunities to intervene earlier.

Similarly, councils are under growing pressure to modernise services, reduce paperwork, and digitise processes. Open Banking also helps here—replacing manual income checks with secure digital consent and reducing the time and administrative burden for staff.

To support those who need it most, local authorities require a faster and more accurate way to assess affordability, which starts with better data.

Open Banking for Local Authorities: A new way to assess poverty

Open Banking for Local Authorities provides a way to assess financial circumstances using live, permissioned data, rather than relying on historic proxies or self-declared forms.

Instead of relying solely on static or self-reported data, councils can use Open Banking to gain insight into the full financial picture. This includes income, spending, debt repayments, and key cost-of-living pressures—all surfaced through a secure and FCA-regulated process and without adding friction to the support process.

It also reduces fraud risk by eliminating the need for self-reported bank statements and removing the chance for document tampering or errors that can delay decisions or lead to poor outcomes.

Here’s how Open Banking supports local authorities:

| Benefit | How Open Banking helps |

| Real-time financial insight | See up-to-date income and spending patterns (not historical or estimated data). |

| Early identification of risk | Spot warning signs like missed bills, rising overdraft use, or reliance on short-term credit. |

| Fairer decision-making | Make consistent, evidence-based decisions grounded in actual affordability. |

| Support for complex cases | Understand irregular income or gig work patterns, which often fall outside traditional metrics. |

| Reduced burden on residents | Residents simply grant secure access via a mobile-friendly link. No need to find, scan or upload documents. It’s faster, easier, and more accessible for those already facing financial or emotional strain. |

With Open Banking, councils can move faster, act earlier, and deliver support where it’s needed most.

Real use cases: From better targeting to better outcomes

With a real-time view of income and spending, local authorities can move from reactive to proactive support. Instead of waiting for residents to reach crisis point—or relying on outdated indicators—councils can identify need earlier, prioritise with confidence, and use their budgets more effectively.

Here are three practical ways Open Banking data is already supporting local government teams:

1. Targeting support programmes more effectively

Whether it’s council tax reductions, discretionary housing payments or cost-of-living grants, Open Banking helps councils pre-qualify applicants with up-to-date affordability data. That means faster decisions, reduced manual workload, and support reaching the right households sooner.

2. Identifying at-risk residents earlier

By spotting signs like rising debt, erratic income, or overdraft reliance, councils can flag residents who may be on the edge of financial hardship—well before they fall behind on payments or request help.

3. Allocating budgets where they’ll have the most impact

With clearer data on who is struggling and by how much, councils can distribute funds more fairly and strategically. It also helps reduce duplication—ensuring multiple teams aren’t unknowingly supporting the same household in silos.

“AperiData and PayPoint’s Customer Support Tool has enabled our advisors to achieve an almost instant, real-time view of people’s financial circumstances, removing barriers to people engaging with debt advice and creating momentum for the people we help to start feeling the benefit.” – Charlotte Blizzard-Welch, CEO at Citizens Advice Stevenage

In fact, some organisations have already reduced financial assessment times from 3 weeks to just 3 minutes—cutting admin while speeding up access to support. See Citizens Advice case study ➝

These use cases are just the starting point. As more councils embed Open Banking into their processes, the potential to improve outcomes—and reduce pressure on frontline teams—only grows.

Data without disruption: Built for local authority realities

Bringing in a new data source shouldn’t mean overhauling your systems or asking already stretched teams to do more. That’s why AperiData is designed to work seamlessly within the operational realities of local government.

Our Open Banking insights enable councils to assess both proof of affordability and proof of poverty in real-time, which is vital for allocating hardship funds, validating discretionary applications, or prioritising support services.

And it goes beyond just adding data. We fill the gaps that traditional CRA sources can’t, especially for residents with thin credit files, irregular incomes, or non-traditional employment. That includes gig workers, carers, and those who may otherwise go unnoticed in standard assessments.

Here’s what sets us apart:

✅Granular, real-time insight: Understand how residents are managing financially—now, not months ago.

✅Purpose-built for local authority use cases: From council tax support to collections and prevention, our data informs decisions across departments.

✅Complements, not replaces, existing data: AperiData enhances your current processes by providing missing context—without disrupting what’s already working.

✅Supports vulnerability identification and fair outcomes: Spot signs of financial stress early and act in line with social value goals.

✅CRA-regulated, public sector-ready: As an FCA-regulated Credit Reference Agency, our solution meets the assurance standards councils increasingly require.

✅Consultative, not transactional: We work closely with your team to ensure integration is simple, insight is actionable, and results are measurable.

✅ Drives operational efficiency: By reducing manual processing and paperwork, AperiData frees up council teams to focus on higher-value support work.

Whether you’re running a pilot or looking to embed Open Banking across your affordability strategy, we’ll help you do it.

Better data, better decisions, better support

When the right data is available—and easy to use—everything changes. Assessments become faster. Support reaches the right households sooner. Resources stretch further.

Open Banking makes it possible. But implementation matters. That’s what AperiData helps local authorities do every day.

If your council is looking to improve how it assesses affordability, prioritises support, or identifies vulnerability, we can help you move quickly and deliver measurable outcomes from day one.

Get in touch to see how AperiData can support your vulnerability strategy.